You can claim UC online

You can claim Universal Credit online – www.gov.uk/apply-universal-credit

Click on the green button that reads ‘Apply now’ to begin.

If you can claim, follow the steps outlined below.

Making a claim can take up to 30 minutes. If you have a partner they will have to make their own separate claim.

You can claim UC online

If you have to make a claim for Universal Credit, then any delay in making the claim could mean that you will miss out on money that you are entitled to. In very limited cases, the DWP will allow up to one month of backdating on a new Universal Credit claim after you submit it. Otherwise, you can only receive an award of Universal Credit from the date you click the ‘submit claim’ button.

So if you need help with your application, ask straight away – the sooner you apply for Universal Credit, the sooner you’ll get your first payment.

If you need help making your claim, you can:

- Contact us.

- Get help from Citizens Advice.

- Call the Universal Credit Helpline: 0800 328 5644.

They can help you make a telephone claim, and may agree to arrange a home visit in certain situations. - Contact your local Job Centre and ask for a list of places locally where you can get help.

I don’t have access to the internet at home

You can usually use a computer for free or access free Wi Fi to make your online claim, in places such as libraries and Jobcentre Plus offices.

Contact us to find out where you can go to get online.

I don’t have an email address

You will need to set up an email address up to be able to claim UC. You can get help if you will find setting up an email address difficult.

I don’t have all the information

Don’t delay in making your claim. If not having the information means you cannot complete the online claim, contact the UC Helpline (0800 328 5644) and ask for help.

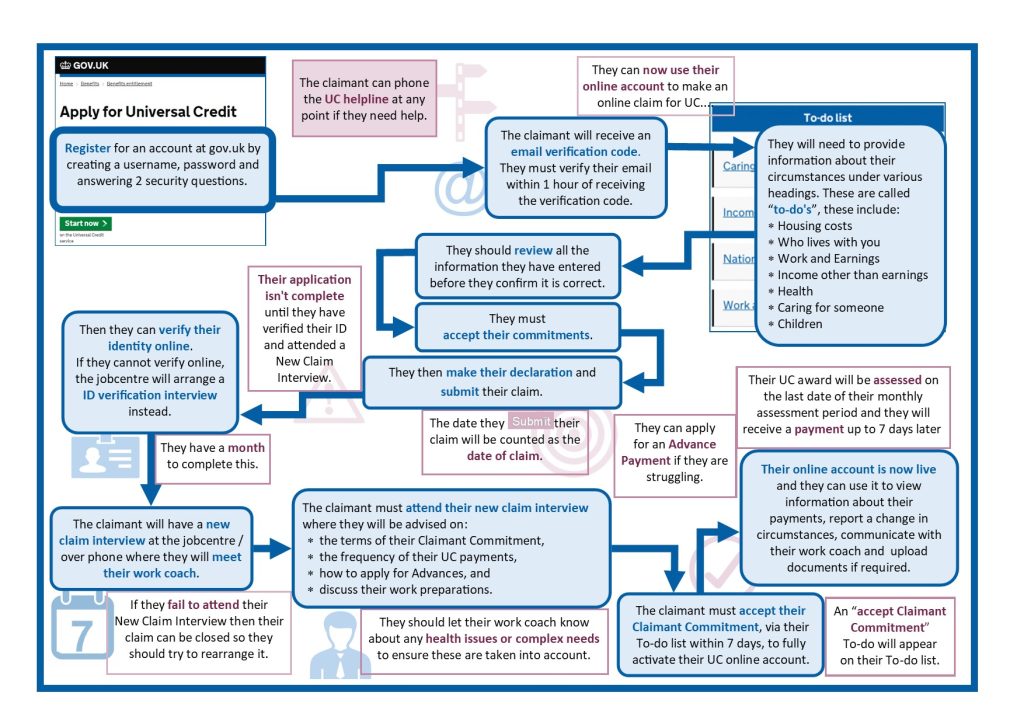

What happens after I’ve claimed online?

After you’ve made your claim for Universal Credit there is still a lot to do to ensure your claim is successful and you get paid.

Once you’ve made your claim you will need to:

- Attend a ‘new claim interview’ – your work coach will contact you to get this booked in so watch out for messages (see below for more information).

- Provide all the evidence and documents requested. If you can’t, you must let your work coach know why.

- If you weren’t able to get your ID verified online, then you will need to attend an ID interview.

- Regularly check your ‘to-do’ list and journal to see if you have any outstanding actions or messages from your Work Coach.

If you are claiming as a couple, you will both need to do the above separately – please see the Claiming as a Couple page.

IMPORTANT: Universal Credit does not include help with your Council Tax bill. You must make a separate claim for Council Tax Reduction from your local council. There should be more details about this on your Council Tax bill.

This is what your claiming journey will look like:

What happens at a new claim interview?

At your new claim interview, your personal ‘Work Coach’ will talk to you about what you need to do to receive Universal Credit. They will confirm whether you are expected to prepare for and/or look for, work.

They will help you draw up a detailed ‘Claimant Commitment’ which sets out what actions you must take to prepare for/look for work. It will explain what will happen if you don’t keep to the terms of your Claimant Commitment.

They will also look at any evidence you have been asked to provide and may ask further questions to make sure the information they have about you and your situation is correct.

Make sure you tell the Work Coach about anything that might cause a problem for you in taking some sort of work. For example, tell them if you have a bad back or if you have difficulty reading or writing. Make sure the Claimant Commitment is something you can keep to.

See The Claimant Commitment page for more information.

IMPORTANT: If you do not attend the new claim interview appointment when required, your claim may be cancelled.

What if I’m not able to make or manage my claim online?

If you have complex needs, a severe disability or other exceptional circumstances that will make it impossible to make and manage your claim online, then ask the DWP to allow you to have a non-digital telephone claim instead.

You (or a friend or family member) will need to ring the Universal Credit Helpline: 0800 328 5644 and explain your difficulties and why this would work better for you.

The DWP are more likely to offer you this service if you:

- Don’t have regular access to the internet.

- Aren’t confident using a computer or smartphone.

- Have problems with your sight.

- Have a long term physical disability or mental health condition which stops you from applying online.

- Have a physical condition that stops you from using a computer or smartphone.

- Can’t read or write.

It can take a while to get through to someone. When you do, tell the person you speak to why you can’t apply online. They’ll ask you some questions to check you’re eligible before going through the next steps of the application with you.

Example:

Shahid lives with his parents. He has been attending his local college but his course is coming to an end. He will then need to claim benefits in his own right. Shahid has learning difficulties and so will not be able to make and maintain an online Universal Credit claim without help. His parents have no experience themselves with using a computer. His sister (who lives locally) calls the UC Helpline and explains the situation. The adviser agrees that it would be best for Shahid to have an offline telephone claim. She helps him make the claim over the phone and explains that he will receive written notifications about his award and can call the UC Helpline to report any changes in his circumstances or ask any questions about his award as he will not have access to an online account.

How to contact the Universal Credit Helpline

Telephone: 0800 328 5644

Textphone: 0800 328 1344

Telephone (Welsh language): 0800 328 1744

Monday to Friday, 8am to 6pm

Calls to these numbers are free.

How to contact Citizen Advice Help to Claim service

Scotland: 0800 023 2581

Calls to these numbers are free.

Advisers are available 8am to 6pm, Monday to Friday.

If you need a British Sign Language interpreter, call the textphone number. An adviser can arrange for an interpreter to translate for you over a video call.